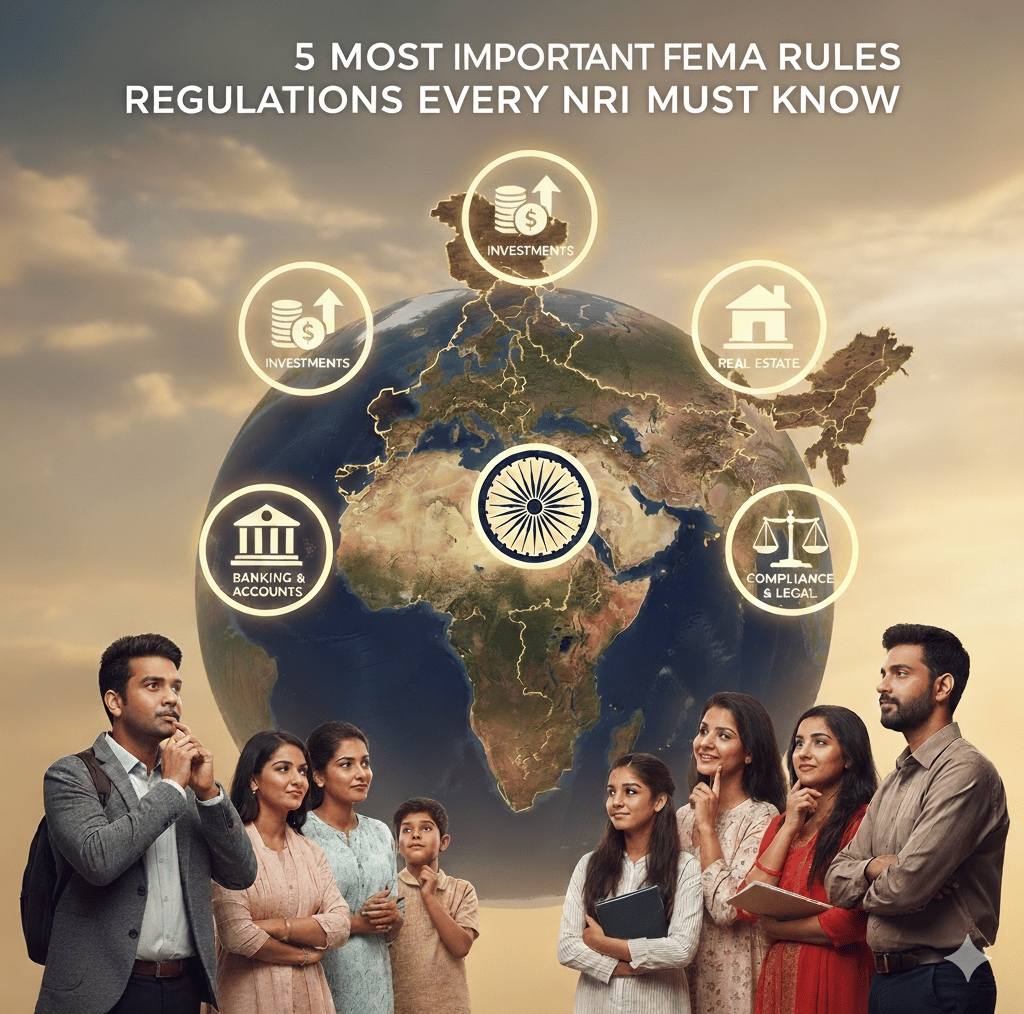

5 Most Important FEMA Rules Every NRI Must Know

The five FEMA must-knows for NRIs: stay compliant while you bank, buy, repatriate, and invest.

FINANCE

9/24/20253 min read

1) FEMA status drives everything: are you “resident outside India”?

Under FEMA, the rules you must follow depend on whether you’re a “person resident in India” or “person resident outside India.” The legal test is in Section 2 of the Foreign Exchange Management Act, 1999—know it before you move money, buy property, or open accounts.

Why it matters: Your status decides which bank accounts you may hold (NRE/NRO/FCNR), what you can buy in India, and how much you can repatriate.

2) The only bank accounts you can legally hold in India as an NRI: NRE, NRO, FCNR(B)

FEMA’s Deposit Regulations permit non-residents to maintain NRE and NRO rupee accounts and FCNR(B) foreign-currency deposits with authorised banks. These rules sit in the Foreign Exchange Management (Deposit) Regulations, 2016 [FEMA 5(R)] and RBI’s consolidated directions/FAQs.

Quick use-case map

NRE (repatriable): Park foreign earnings; principal + interest fully repatriable.

NRO (generally non-repatriable): Use for Indian-source income (rent/dividends). Limited repatriation allowed—see Rule #3 below.

FCNR(B) (repatriable): Fixed deposits in permitted foreign currencies.

(See RBI FAQs for permissible credits/debits and joint holding variants.)

Important conversion rule: When your status changes from resident → NRI, your existing resident savings/current account must be redesignated as an NRO (you can’t legally keep a normal resident account). RBI says this explicitly in its official FAQ.

3) Getting money out: the USD 1 million repatriation window from NRO and sale proceeds

FEMA allows NRIs/OCIs to remit out of India up to USD 1,000,000 per financial year from NRO balances and certain asset sale proceeds, subject to documentation and taxes. The framework is the Foreign Exchange Management (Remittance of Assets) Regulations, 2016 [FEMA 13(R)] and RBI Master Direction No. 13 (Remittance of Assets).

RBI’s NRO/Remittance guidance also reiterates the USD 1M limit and documentary requirements (including CA certification per CBDT formats). Build your repatriation plan around this cap.

4) Buying and selling property in India: what NRIs/OCIs can—and cannot—do

Your rights to acquire/transfer immovable property are set out in FEMA 21(R) — Acquisition and Transfer of Immovable Property in India Regulations, 2018, plus RBI’s official FAQs (consolidated under Master Direction No. 12). Core rules:

You may purchase residential/commercial property, but you cannot purchase agricultural land, plantation property, or a farmhouse.

Pay only through banking channels (or from NRE/FCNR(B)/NRO balances)—no cash/traveller’s cheques.

Repatriating sale proceeds is allowed subject to conditions; if the property was bought with foreign-currency/NRE/FCNR funds, repatriation is generally limited to the original investment amount, and for residential property, sale-proceeds repatriation is restricted to not more than two such properties.

(For edge cases—inheritance, LTV holders, or restricted nationalities—the RBI FAQ spells out the specific carve-outs and approvals.)

5) Investing in Indian securities: repatriable vs non-repatriable routes

NRI/OCI investment into Indian equity and other non-debt instruments is now primarily governed by the FEMA (Non-Debt Instruments) Rules, 2019 and RBI’s Master Direction – Foreign Investment in India. In short:

On a repatriation basis: You may purchase/sell listed equity and other permitted instruments, subject to sectoral caps and the automatic/approval routes.

On a non-repatriation basis: Additional avenues exist, but proceeds are generally not freely repatriable.

Always check sector-specific conditions and reporting (e.g., Form FC-TRS/FC-GPR).

Handy compliance checklist (save this)

Status check: Confirm your FEMA residential status annually.

Banking hygiene: Convert resident accounts to NRO on becoming NRI; use NRE/FCNR(B) for foreign earnings.

Repatriation plan: Budget within the USD 1M NRO window each financial year; keep proofs and CA certificate ready.

Property rules: Don’t buy agricultural/plantation/farmhouse; follow permitted payment modes; mind the two-residential-property sale-proceeds repatriation cap.

Investments: Use the right route (repatriable/non-repatriable) and file reports as required.

Official FEMA/RBI links to bookmark (per rule above)

FEMA Act (definitions & powers): India Code – Foreign Exchange Management Act, 1999 (sections 2(v), 2(w)).

Deposits (NRE/NRO/FCNR): FEMA 5(R) text (Govt. portal) and RBI’s Deposits/Accounts FAQs.

Remittance of Assets (USD 1M rule): RBI Master Direction No. 13 + RBI FAQ page.

Property: FEMA 21(R) regulations (Official PDF) + RBI Property FAQs (Master Direction No. 12 reference).

Investments: FEMA Non-Debt Instruments Rules, 2019 + RBI Master Direction – Foreign Investment in India.

Final word, the LBI way

Think of FEMA as your rulebook for living financially “bi-country.” Nail your status, keep the right accounts, repatriate with a paper trail, follow the property playbook, and invest through the correct route. Do these five things right and you’ll avoid 99% of avoidable headaches as an NRI.

*Disclaimer: Life Beyond India shares educational content only. We are not a SEBI-registered investment adviser/financial advisor. Please don’t treat this as financial advice—speak with a qualified professional before making decisions.

Support

Subscribe

contact@lifebeyondindia.com

© 2025. All rights reserved.

*Disclaimer: Life Beyond India (“the Blog”) provides content for educational and informational purposes only. The author is not a SEBI-registered investment adviser (RIA) or financial advisor, and no content on this site should be considered financial, investment, legal, or tax advice. While we aim to keep information accurate and current, we cannot guarantee completeness or timeliness, and regulations can change without notice. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

Before making any financial decision, seek advice from a qualified professional—for example, a SEBI-registered investment adviser in India and/or an appropriately licensed advisor in your country of residence who can consider your specific goals, risk tolerance, and personal circumstances. By using this Blog, you agree that you bear full responsibility for your financial decisions and that the author and the Blog are not liable for any actions taken based on the information provided here.